)

| Online Credit Card Processing | Back Forward Print this topic |

Online Credit Card processing option is available to U.S. based subscribers only.

Need Online Credit Card Processing?

MyFBO Advanced Edition and AvPOS Edition Subscribers have the ability to process credit cards online through the online system.

What do I Need?

To process credits cards online through the MyFBO system you will need a merchant account and an IP Gateway. With the MyFBO system both the IP Gateway and Merchant Account are provided by AHT Gateway, a sister company.

What is a Merchant Account?

A merchant account is an account provided by a financial institution that allows your company to accept credit cards. Merchant accounts have an underwriting process.

What is an IP Gateway?

An IP Gateway enables you to authorize, settle, and manage credit card transactions from your location using the speed and security of the Internet. Although everything appears seamless and linked together, an IP Gateway is a separate virtual device to your merchant account.

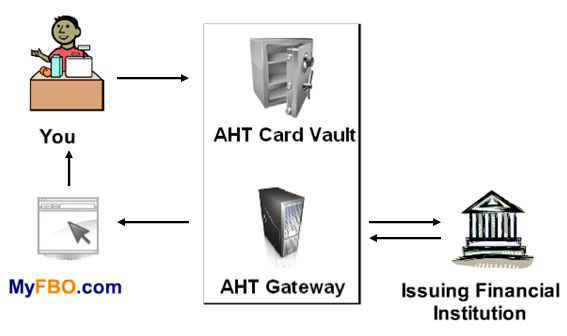

How does it Work?

The basic illustration below shows the process. Essentially when you swipe or key enter a card in MyFBO, the card information is sent from your browser to the AHT Gateway IP Gateway. The gateway software then stores the card if requested and/or sends the card off to the issuing financial institution. The issuing financial institution will send back an approved or declined message. The AHT Gateway IP Gateway then will let you and the MyFBO software know if the card was approved. If you choose to store the card on file in the AHT Gateway IP Gateway then a token is also sent to the MyFBO software. The token is used as a reference to that card in the vault. Tokens are used instead of actual card numbers for security purposes and to maintain PCI Compliance.

How do I get Money?

After you run a card and it is settled, the funds are deposited into your bank account. You can bank anywhere you like. The processors will usually deposit into any standard business checking account. Funds from Visa, MasterCard, and Discover charges are normally received within 2 to 3 business days. American Express usually takes 3 business days but can take up to 5 business days. Multi-Service®, AVCARD®, contract fuel, and oil company cards may take longer to settle.

Funds are usually deposited and then credit card fees are then immediately withdrawn, although the fee collection process can vary.

Types of Cards

The types of cards that you accept depend on whether you're a fuel dealer or not. Schools, clubs, and other businesses accept certain consumer cards. If you are a fuel dealer you will also accept certain fuel cards and branded cards. Fuel dealer accounts are set up differently. Fuel dealers should contact MyFBO Support prior to the application process.

Consumer cards are Visa, MasterCard, Discover, and American Express. Generally when you sign up for a merchant account Visa, MasterCard, and Discover are bundled together. If you wish to accept American Express cards you will need to check that off on the application.

Before you make a decision on what types of cards to accept, here are some statistics from the FDIC*:

| Card | Percentage of Transactions in U.S. |

| Visa and MasterCard | 70% |

| American Express | 23% |

| Discover | 7% |

*Source FDIC.gov

Credit Card Fees and Costs

Fees are charged each time a card is processed. Fees depend upon the type of card, type of business, and how the card is processed. For example, Visa and MasterCard generally have a lower fee than American Express. "Rewards" cards such as cash back and frequent flyer cards can charge higher fees as well. If the card is "swiped" or "key-entered" can also make a difference.

Estimated costs and fees are outlined below. Note that MyFBO is not in the credit card business and we make no money from your card processing. Please refer questions about fees and rates to the processor (AHT Gateway).

Rates shown are subject to change.

How the Fees Compare

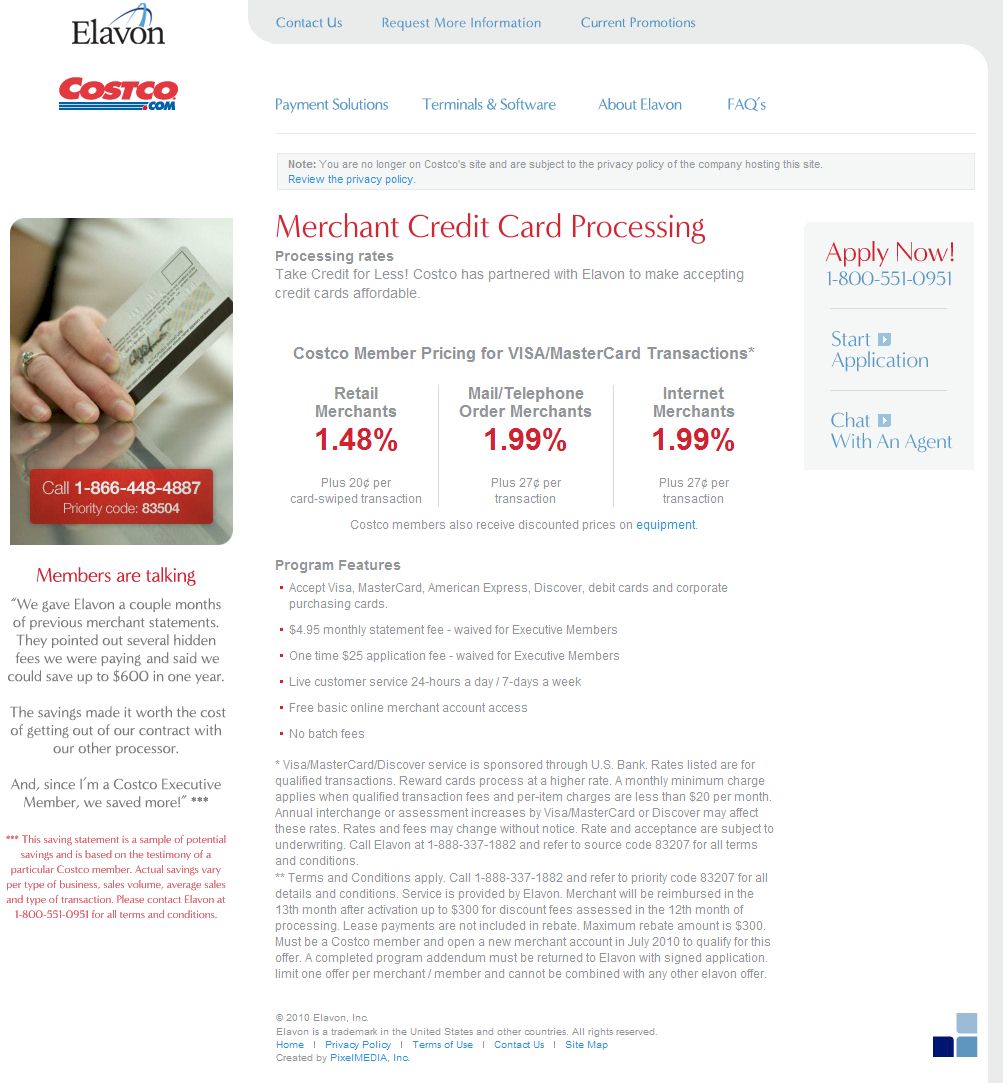

The rates above may sound high but are competitive. The key to credit card fees is looking at them as a whole. Many providers will advertise much lower rates but have a lot of hidden fees. For example, Costco.com (http://www.elavon.com/acquiring/costco/) advertises an online processing rate of 1.48% (in dark red) plus 20 cents per transaction (in light gray). This sounds like a great rate but when you read the fine print (in light gray) there are statement fees, monthly minimum fees, some strange rebate deal, and the whole thing does not include a PCI Compliant IP Gateway which would cost extra.

What is PCI Compliance?

PCI is the Payment Card Industry. It is a consortium between Visa�, MasterCard�, Discover�, American Express�, and JCB�. The PCI developed a new set of standards to assist merchants and service providers in maintaining card data security. You will, or have, committed to abide by these standards in the agreement with your merchant services provider. In other words, to accept their cards you have to play by their new rules.

The goods news is that MyFBO and AHT Gateway have done most of the work for you. Subscribers using the AHT Gateway can self-certify, saving tens of thousands of dollars. Many of the requirements in the PCI standard are "check offs" as a result of the work done by MyFBO and AHT Gateway. However, there are requirements where you must take action or verify compliance, but MyFBO provides the documentation to "walk you through it". Click here for more information about PCI Compliance.

Merchant Account Underwriting and Risk

Merchant account providers are liable for losses. Since consumers can dispute any charge on their credit card for 6 months, the losses can be substantial. This means that before they provide you with a merchant account they decide whether new accounts (you) are worth the risk. This decision process is the underwriting process. The type of industry, the way you process, and volume changes your risk profile. Here are some keys to reducing your risk:

Volume

The key thing with credit card sales volume is not to overstate it. If you put $10,000 per month in Visa and MasterCard sales on your application, the merchant account provider has to underwrite 6 months or $60,000.

Overstating your volume on the application does not get you a better rate, it will just slow the application process down and increases the chances that you will be denied an account. For example, in the example above the underwriters will be checking your credit to see if it can withstand a $60,000 "hit".

If you already have a merchant account somewhere else, it makes the underwriting process easier. Be prepared to provide the last 3 months of statements. It shows the underwriters someone else took a risk on your business and it paid off.

Largest Ticket

Another risk issue is your highest ticket. Credit cards are not meant to be used for big ticket items. You probably shouldn't put down more than a $5,000 highest ticket on your application. For example, if you put down a highest ticket of $10,000 then the underwriters assume you could potentially charge $300,000 before anyone catches any fraud.

Industry Risk

Not all "aviation" companies are created equal. It is important to realize airports and fuel dealers are a higher risk than flight schools. In other words if you are primarily a flight school you should put that on the application and do not just put "FBO" unless you are an FBO of course.

Account Risk

Avoid life-time memberships, annual billing, and large amounts on account if you can. If you bill this way you will have to show that you have good financials to back up the account risk.

Percentage of your Transactions not Swiped

This should be less than 20% on your application. Risk goes way up if this exceeds 20%. If the cardholder is in front of you, you should swipe (even if their card is on file in the vault).

Personal Guarantee

Just for your information the merchant account providers will need you and any partners to sign a personal guarantee. They will want to do credit checks on each partner. This is an industry standard practice.

Advantages to Online Credit Card Processing

At this point credit processing may be confusing. Hopefully this document helped explain the process. If you are asking yourself "why bother", below are some good reasons.

Why AHT Gateway?

One Final Word to the Wise

No matter which card processing options you choose, always independently verify and read contracts well. Also, once you have card processing, balance your accounts to ensure you are getting paid!

More Information / Get Started

To get started you will need a Merchant Account and Gateway provided by AHT. For more information, please contact:

| Copyright © MyFBO.com [email protected] |

06/18/13 clil

)