General Journal Entries

The Online System contains a General or Plain Language Journal Entries Report

on the Accounting / Interface Menu. The General Journal Entries is

the simplest and easiest way to interface with external accounting programs such

as QuickBooks®.

To run the report, select a starting date,

ending date, and a location (for multi-location operators), and then click the

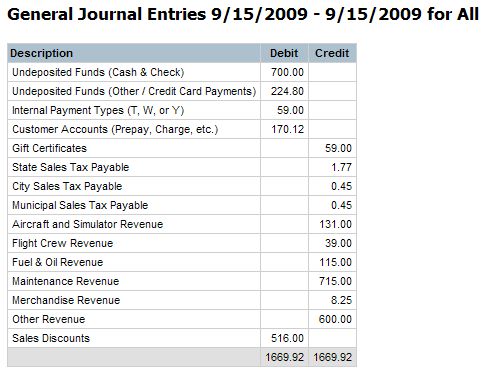

Go button. The Journal Entry Report is a summary and has 16 possible items:

- Un-deposited Funds (Cash & Check) - Total Cash and Check

payments you received for the given date range. This account usually has a

debit balance.

- Un-deposited Funds (Other / Credit Card Payments) - Total other

payments you received for the given date range. Other payments are usually

credit card payments. This is a separate line on the report because

sometimes further accounting is required, such as expensing credit card

fees. This account usually has a debit balance.

- Internal Payment Types (T, W, or Y) - Internal payment types from

the Payment and Card Type parameters. Types T, W, and Y do not appear in

Online System's cash drawer. For example, many Subscribers use these payment

types to "write off" a transaction. If this is the case at your

operation, you could debit a "bad debt expense" or similar account

in your external accounting software. This account usually has a debit

balance.

- Customer Accounts (Prepay, Charge, etc.) - Sum of customer

accounts. Customer accounts can include Prepay, Charge, Special, and Urgent.

This line could have a debit or credit balance depending on the types of

accounts and how they change position. For example, a prepay balance is a

liability and increased with a credit. When a customer uses some of their

prepaid funds, the liability is reduced with a debit. Here is how a

prepayment account journal entry breaks down:

Cash (Asset) = Debit

Prepaid Account (Liability or Negative A/R) = Credit

Explanation: Customer Funds Account

Prepaid Account (Liability or Negative A/R Reduced) = Debit

Revenue = Credit

Explanation: Customer uses Funds

The reverse is true for charge accounts. Note, in most external accounting programs,

Customer Accounts is setup as an Accounts Receivable (A/R) Account.

External accounting programs seem to handle negative Accounts Receivable

better than they handle a positive Accounts Payable.

- Gift Certificates - Sum of gift certificate sales and redemptions

for the given date range. This line could have a debit or credit balance.

When a gift certificate is sold, it is a liability, and when it is redeemed, it

is revenue. Here is how it breaks down:

Cash (Asset) = Debit

Gift Certificate (Liability) = Credit

Explanation: Gift Certificate Sold

Gift Certificate (Liability Removed) = Debit

Revenue = Credit

Explanation: Gift Certificate Redeemed

- State Sales Tax Payable - Sum of sales taxes charged and collected.

Usually a credit balance.

- City Sales Tax Payable - Sum of city sales taxes charged and

collected (if local taxes enabled in your system). Usually a credit balance.

- Municipal Sales Tax Payable - Sum of municipal sales taxes charged

and collected (if local taxes enabled in your system). Usually a credit

balance.

- Aircraft and Simulator Revenue - Sum of revenues associated with

aircraft and simulator operations. Usually a credit balance.

- Flight Crew Revenue - Sum of revenues associated with staff.

Usually charter pilots and flight instructors. Usually a credit balance.

- Fuel & Oil Revenue - Sum of revenues associated with fuel and

oil. Usually a credit balance.

- Maintenance Revenue - Sum of revenues associated maintenance, such

as maintenance labor and parts. Usually a credit balance.

- Merchandise Revenue - Sum of revenues for merchandise sold. Usually

a credit balance.

- Other Revenue - Sum of revenues for any items sold, not

associated with a revenue account above, such as "general

revenue". Usually a credit balance.

- Sales Discounts - Sales discounts or credits from the receipts.

These can include special offers, rebates, and general credits. Usually a

debit balance. Sales discounts is a contra-revenue account.

- Cash Expenditures - Appears if you allow cash expenditures from

your cash drawer and if you have a cash expenditure. Many times this is

handled as "petty cash". Usually a debit

balance.

The Journal Entry Report also has a total at the bottom. If the sum of the

debits does not match the sum of the credits, a red "Out

of Balance" message will appear. If the report is out of

balance, it is likely someone managed to do something weird while creating a

receipt.

General Journal Entries Report

09/01/09 P